- Học kỳ

- SP2026

- Thời Gian

- 3/5/26

- Loại tài liệu

- FE

FIN306c SP26 FE RE

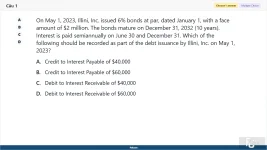

1. (Choose 1 answer)

On May 1, 2023, Illini, Inc. issued 6% bonds at par, dated January 1, with a face amount of $2 million. The bonds mature on December 31, 2032 (10 years). Interest is paid semiannually on June 30 and December 31. Which of the following should be recorded as part of the debt issuance by Illini, Inc. on May 1, 2023?

A. Credit to Interest Payable of $40,000

B. Credit to Interest Payable of $60,000

C. Debit to Interest Receivable of $40,000

D. Debit to Interest Receivable of $60,000

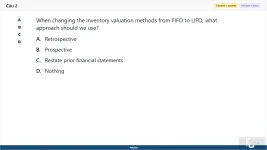

2. (Choose 1 answer)

When changing the inventory valuation methods from FIFO to LIFO, what approach should we use?

A. Retrospective

B. Prospective

C. Restate prior financial statements

D. Nothing

3. (Choose 1 answer)

Which of the following statements is not correct when comparing a cash flow statement prepared using the direct method versus a cash flow statement prepared using the indirect method?

A. Both have identical financing activities section.

B. Both have identical investing activities section.

C. Both have identical operating activities section.

D. Both have three sections.

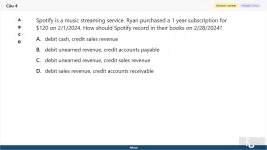

4. (Choose 1 answer)

Spotify is a music streaming service. Ryan purchased a 1 year subscription for $120 on 2/1/2024. How should Spotify record in their books on 2/28/2024?

A. debit cash, credit sales revenue

B. debit unearned revenue, credit accounts payable

C. debit unearned revenue, credit sales revenue

D. debit sales revenue, credit accounts receivable

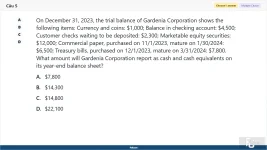

5. (Choose 1 answer)

On December 31, 2023, the trial balance of Gardenia Corporation shows the following items: Currency and coins: $1,000; Balance in checking account: $4,500; Customer checks waiting to be deposited: $2,300; Marketable equity securities: $12,000; Commercial paper, purchased on 11/1/2023, mature on 1/30/2024: $6,500; Treasury bills, purchased on 12/1/2023, mature on 3/31/2024: $7,800. What amount will Gardenia Corporation report as cash and cash equivalents on its year-end balance sheet?

A. $7,800

B. $14,300

C. $14,800

D. $22,100

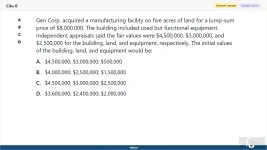

6. (Choose 1 answer)

Gen Corp. acquired a manufacturing facility on five acres of land for a lump-sum price of $8,000,000. The building included used but functional equipment. Independent appraisals said the fair values were $4,500,000, $3,000,000, and $2,500,000 for the building, land, and equipment, respectively. The initial values of the building, land, and equipment would be:

A. $4,500,000; $3,000,000; $500,000

B. $4,000,000; $2,500,000; $1,500,000

C. $4,500,000; $3,000,000; $2,500,000

D. $3,600,000; $2,400,000; $2,000,000

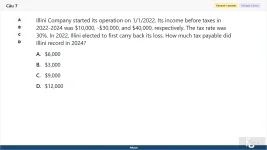

7. (Choose 1 answer)

Illini Company started its operation on 1/1/2022. Its income before taxes in 2022-2024 was $10,000, -$30,000, and $40,000, respectively. The tax rate was 30%. In 2022, Illini elected to first carry back its loss. How much tax payable did Illini record in 2024?

A. $6,000

B. $3,000

C. $9,000

D. $12,000

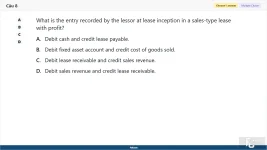

8. (Choose 1 answer)

What is the entry recorded by the lessor at lease inception in a sales-type lease with profit?

A. Debit cash and credit lease payable.

B. Debit fixed asset account and credit cost of goods sold.

C. Debit lease receivable and credit sales revenue.

D. Debit sales revenue and credit lease receivable.

9. (Choose 1 answer)

Illini Company issued $1,000,000 3-year 8% convertible bonds on January 1, 2022 for $1,000,000. Each $1,000 bond can be converted into 50 shares of Illini's common stock. The fair value of Illini's common stock was $22 per share on January 1, 2022. What is the value of the beneficial conversion feature at January 1, 2022?

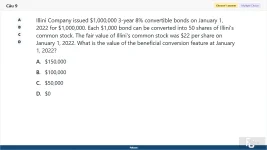

A. $150,000

B. $100,000

C. $50,000

D. $0

10. (Choose 1 answer)

The fixed asset turnover ratio is a financial metric that measures:

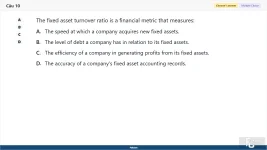

A. The speed at which a company acquires new fixed assets.

B. The level of debt a company has in relation to its fixed assets.

C. The efficiency of a company in generating profits from its fixed assets.

D. The accuracy of a company's fixed asset accounting records.

11. (Choose 1 answer)

ABC Corporation has been using the FIFO inventory valuation method for several years. They have decided to switch to the LIFO method in the current year. Which accounting principle requires that they disclose this change in their financial statements?

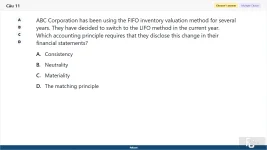

A. Consistency

B. Neutrality

C. Materiality

D. The matching principle

12. (Choose 1 answer)

Which of the following statements accurately describes the difference between revenue recognition at a certain point in time and revenue recognition over a period of time?

A. Revenue recognition at a certain point in time recognizes revenue based on the transfer of control, while revenue recognition over a period of time recognizes revenue when cash is received.

B. Revenue recognition at a certain point in time and revenue recognition over a period of time are the same concepts and do not have any differences.

C. Revenue recognition at a certain point in time recognizes revenue when goods or services are delivered, while revenue recognition over a period of time recognizes revenue proportionally over the duration of a long-term contract.

D. Revenue recognition at a certain point in time recognizes revenue when cash is received, while revenue recognition over a period of time recognizes revenue when the right to receive payment is established.

13. (Choose 1 answer)

The interest expense for the reporting period on a bond is calculated using _________ rate and the cash payments are calculated using _________ rate.

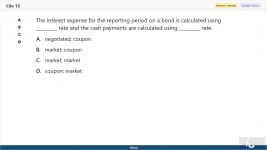

A. negotiated; coupon

B. market; coupon

C. market; market

D. coupon; market

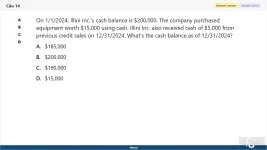

14. (Choose 1 answer)

On 1/1/2024, Illini Inc.'s cash balance is $200,000. The company purchased equipment worth $15,000 using cash. Illini Inc. also received cash of $5,000 from previous credit sales on 12/31/2024. What's the cash balance as of 12/31/2024?

A. $185,000

B. $200,000

C. $190,000

D. $15,000

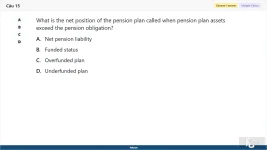

15. (Choose 1 answer)

What is the net position of the pension plan called when pension plan assets exceed the pension obligation?

A. Net pension liability

B. Funded status

C. Overfunded plan

D. Underfunded plan

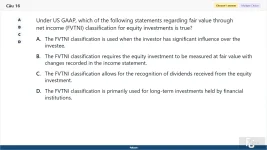

16. (Choose 1 answer)

Under US GAAP, which of the following statements regarding fair value through net income (FVTNI) classification for equity investments is true?

A. The FVTNI classification is used when the investor has significant influence over the investee.

B. The FVTNI classification requires the equity investment to be measured at fair value with changes recorded in the income statement.

C. The FVTNI classification allows for the recognition of dividends received from the equity investment.

D. The FVTNI classification is primarily used for long-term investments held by financial institutions.

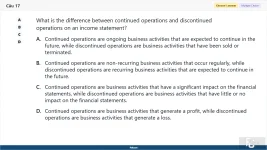

17. (Choose 1 answer)

What is the difference between continued operations and discontinued operations on an income statement?

A. Continued operations are ongoing business activities that are expected to continue in the future, while discontinued operations are business activities that have been sold or terminated.

B. Continued operations are non-recurring business activities that occur regularly, while discontinued operations are recurring business activities that are expected to continue in the future.

C. Continued operations are business activities that have a significant impact on the financial statements, while discontinued operations are business activities that have little or no impact on the financial statements.

D. Continued operations are business activities that generate a profit, while discontinued operations are business activities that generate a loss.

18. (Choose 1 answer)

When the effective interest rate of a bond is larger than its stated (or nominal) interest rate, the bond would be sold:

A. at a discount.

B. at a premium.

C. at the face amount.

D. at an unknown value.

19. (Choose 1 answer)

The selling price for a two-year warranty is $500, and the selling price for a laptop is $1,000. In order to attract more customers, the store manager decided to introduce the bundle price of $1,200. How should the store record the journal entry for the above transaction?

A. debit cash 1200, credit sales revenue 1200

B. debit cash 1200, credit sales revenue 800, credit unearned revenue 400

C. debit accounts receivable 1200, credit unearned revenue 1200

D. debit cash 1500, credit sales revenue 1200, credit unearned revenue 300

20. (Choose 1 answer)

ABC Company has been using the Average Cost inventory method for several years but is considering changing to the LIFO (Last-In, First-Out) method. Which of the following statements is a potential advantage of switching to the LIFO method?

A. LIFO provides a better reflection of the physical flow of inventory.

B. LIFO enhances financial statement comparability across different companies.

C. LIFO simplifies recordkeeping and cost calculations.

D. LIFO results in lower taxable income during periods of rising prices.

21. (Choose 1 answer)

What is the purpose of "amortizing the differential" in the equity method?

A. To consolidate financial statements

B. To account for disparities between reported net income and consolidation procedures

C. To adjust the fair value of investment shares

D. To calculate the book value of the underlying net assets acquired

22. (Choose 1 answer)

Which of the following is true regarding the expected return on plan assets under IFRS?

A. It is assumed to be equal to the actuary's discount rate.

B. It is estimated based on the underlying investments.

C. It is recorded as a separate line item in the income statement.

D. It is excluded from pension accounting calculations.

23. (Choose 1 answer)

Which of the following is an example of a temporary difference that can lead to a deferred tax asset?

A. Unrealized gains on certain investments

B. Recognition of an accrued expense on the income statement

C. Recognition of revenues related to cash collected in a prior period

D. Payment of prepaid expenses for financial reporting

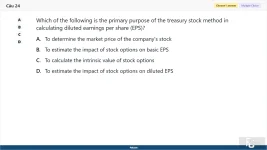

24. (Choose 1 answer)

Which of the following is the primary purpose of the treasury stock method in calculating diluted earnings per share (EPS)?

A. To determine the market price of the company's stock

B. To estimate the impact of stock options on basic EPS

C. To calculate the intrinsic value of stock options

D. To estimate the impact of stock options on diluted EPS

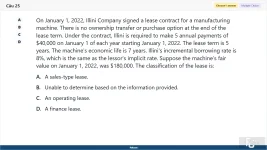

25. (Choose 1 answer)

On January 1, 2022, Illini Company signed a lease contract for a manufacturing machine. There is no ownership transfer or purchase option at the end of the lease term. Under the contract, Illini is required to make 5 annual payments of $40,000 on January 1 of each year starting January 1, 2022. The lease term is 5 years. The machine's economic life is 7 years. Illini's incremental borrowing rate is 8%, which is the same as the lessor's implicit rate. Suppose the machine's fair value on January 1, 2022, was $180,000. The classification of the lease is:

A. A sales-type lease.

B. Unable to determine based on the information provided.

C. An operating lease.

D. A finance lease.

26. (Choose 1 answer)

What is the purpose of the vesting period in share-based compensation?

A. To determine the period over which expense will be recorded

B. To determine the market value of the company's stock

C. To calculate the tax implications of share-based awards

D. To establish the eligibility criteria for employees

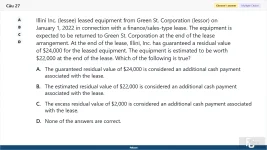

27. (Choose 1 answer)

Illini Inc. (lessee) leased equipment from Green St. Corporation (lessor) on January 1, 2022 in connection with a finance/sales-type lease. The equipment is expected to be returned to Green St. Corporation at the end of the lease arrangement. At the end of the lease, Illini, Inc. has guaranteed a residual value of $24,000 for the leased equipment. The equipment is estimated to be worth $22,000 at the end of the lease. Which of the following is true?

A. The guaranteed residual value of $24,000 is considered an additional cash payment associated with the lease.

B. The estimated residual value of $22,000 is considered an additional cash payment associated with the lease.

C. The excess residual value of $2,000 is considered an additional cash payment associated with the lease.

D. None of the answers are correct.

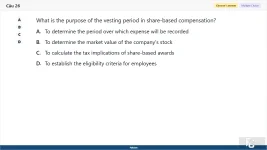

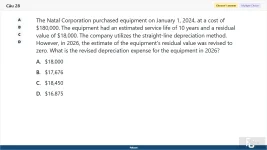

28. (Choose 1 answer)

The Natal Corporation purchased equipment on January 1, 2024, at a cost of $180,000. The equipment had an estimated service life of 10 years and a residual value of $18,000. The company utilizes the straight-line depreciation method. However, in 2026, the estimate of the equipment's residual value was revised to zero. What is the revised depreciation expense for the equipment in 2026?

A. $18,000

B. $17,676

C. $18,450

D. $16,875

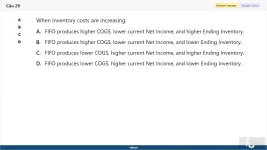

29. (Choose 1 answer)

When inventory costs are increasing:

A. FIFO produces higher COGS, lower current Net Income, and higher Ending Inventory.

B. FIFO produces higher COGS, lower current Net Income, and lower Ending Inventory.

C. FIFO produces lower COGS, higher current Net Income, and higher Ending Inventory.

D. FIFO produces lower COGS, higher current Net Income, and lower Ending Inventory.

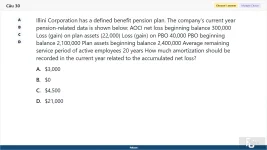

30. (Choose 1 answer)

Illini Corporation has a defined benefit pension plan. The company's current year pension-related data is shown below: AOCI net loss beginning balance 300,000 Loss (gain) on plan assets (22,000) Loss (gain) on PBO 40,000 PBO beginning balance 2,100,000 Plan assets beginning balance 2,400,000 Average remaining service period of active employees 20 years How much amortization should be recorded in the current year related to the accumulated net loss?

A. $3,000

B. $0

C. $4,500

D. $21,000

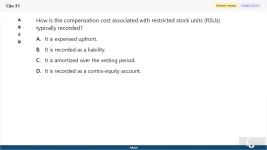

31. (Choose 1 answer)

How is the compensation cost associated with restricted stock units (RSUs) typically recorded?

A. It is expensed upfront.

B. It is recorded as a liability.

C. It is amortized over the vesting period.

D. It is recorded as a contra-equity account.

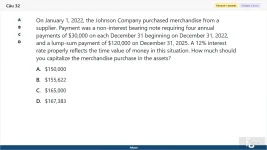

32. (Choose 1 answer)

On January 1, 2022, the Johnson Company purchased merchandise from a supplier. Payment was a non-interest bearing note requiring four annual payments of $30,000 on each December 31 beginning on December 31, 2022, and a lump-sum payment of $120,000 on December 31, 2025. A 12% interest rate properly reflects the time value of money in this situation. How much should you capitalize the merchandise purchase in the assets?

A. $150,000

B. $155,622

C. $165,000

D. $167,383

33. (Choose 1 answer)

What are the rights typically granted to common shareholders?

A. Preferred dividends and higher claim to a company's assets

B. Voting rights, share in profits, and share in asset distribution

C. Ability to convert preferred shares to common stock

D. Ability to redeem shares for a fixed amount

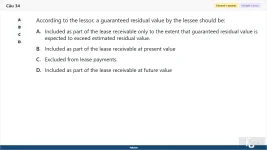

34. (Choose 1 answer)

According to the lessor, a guaranteed residual value by the lessee should be:

A. Included as part of the lease receivable only to the extent that guaranteed residual value is expected to exceed estimated residual value.

B. Included as part of the lease receivable at present value

C. Excluded from lease payments.

D. Included as part of the lease receivable at future value

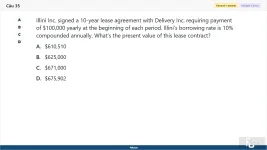

35. (Choose 1 answer)

Illini Inc. signed a 10-year lease agreement with Delivery Inc. requiring payment of $100,000 yearly at the beginning of each period. Illini's borrowing rate is 10% compounded annually. What's the present value of this lease contract?

A. $610,510

B. $625,000

C. $671,000

D. $675,902

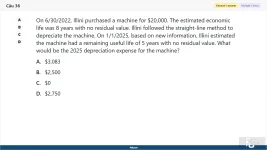

36. (Choose 1 answer)

On 6/30/2022, Illini purchased a machine for $20,000. The estimated economic life was 8 years with no residual value. Illini followed the straight-line method to depreciate the machine. On 1/1/2025, based on new information, Illini estimated the machine had a remaining useful life of 5 years with no residual value. What would be the 2025 depreciation expense for the machine?

A. $3,083

B. $2,500

C. $0

D. $2,750

37. (Choose 1 answer)

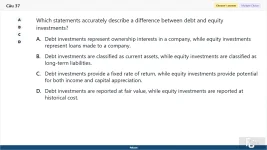

Which statements accurately describe a difference between debt and equity investments?

A. Debt investments represent ownership interests in a company, while equity investments represent loans made to a company.

B. Debt investments are classified as current assets, while equity investments are classified as long-term liabilities.

C. Debt investments provide a fixed rate of return, while equity investments provide potential for both income and capital appreciation.

D. Debt investments are reported at fair value, while equity investments are reported at historical cost.

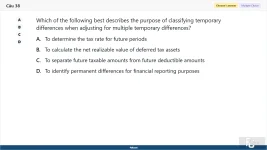

38. (Choose 1 answer)

Which of the following best describes the purpose of classifying temporary differences when adjusting for multiple temporary differences?

A. To determine the tax rate for future periods

B. To calculate the net realizable value of deferred tax assets

C. To separate future taxable amounts from future deductible amounts

D. To identify permanent differences for financial reporting purposes

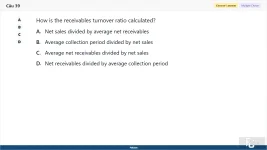

39. (Choose 1 answer)

How is the receivables turnover ratio calculated?

A. Net sales divided by average net receivables

B. Average collection period divided by net sales

C. Average net receivables divided by net sales

D. Net receivables divided by average collection period

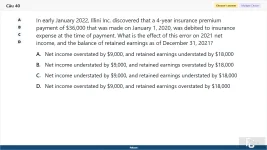

40. (Choose 1 answer)

In early January 2022, Illini Inc. discovered that a 4-year insurance premium payment of $36,000 that was made on January 1, 2020, was debited to insurance expense at the time of payment. What is the effect of this error on 2021 net income, and the balance of retained earnings as of December 31, 2021?

A. Net income overstated by $9,000, and retained earnings understated by $18,000

B. Net income understated by $9,000, and retained earnings overstated by $18,000

C. Net income understated by $9,000, and retained earnings understated by $18,000

D. Net income overstated by $9,000, and retained earnings overstated by $18,000

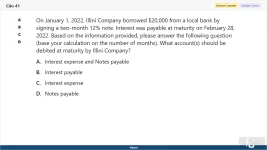

41. (Choose 1 answer)

On January 1, 2022, Illini Company borrowed $20,000 from a local bank by signing a two-month 12% note. Interest was payable at maturity on February 28, 2022. Based on the information provided, please answer the following question (base your calculation on the number of months). What account(s) should be debited at maturity by Illini Company?

A. Interest expense and Notes payable

B. Interest payable

C. Interest expense

D. Notes payable

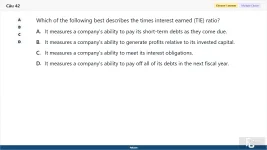

42. (Choose 1 answer)

Which of the following best describes the times interest earned (TIE) ratio?

A. It measures a company's ability to pay its short-term debts as they come due.

B. It measures a company's ability to generate profits relative to its invested capital.

C. It measures a company's ability to meet its interest obligations.

D. It measures a company's ability to pay off all of its debts in the next fiscal year.

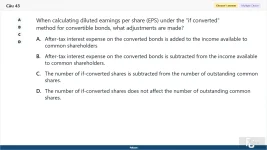

43. (Choose 1 answer)

When calculating diluted earnings per share (EPS) under the "if converted" method for convertible bonds, what adjustments are made?

A. After-tax interest expense on the converted bonds is added to the income available to common shareholders

B. After-tax interest expense on the converted bonds is subtracted from the income available to common shareholders.

C. The number of if-converted shares is subtracted from the number of outstanding common shares.

D. The number of if-converted shares does not affect the number of outstanding common shares.

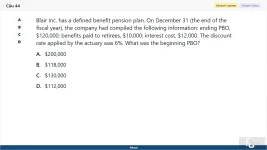

44. (Choose 1 answer)

Blair Inc. has a defined benefit pension plan. On December 31 (the end of the fiscal year), the company had compiled the following information: ending PBO, $120,000; benefits paid to retirees, $10,000; interest cost, $12,000. The discount rate applied by the actuary was 6%. What was the beginning PBO?

A. $200,000

B. $118,000

C. $130,000

D. $112,000

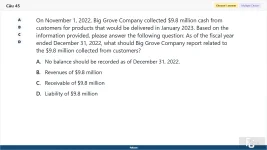

45. (Choose 1 answer)

On November 1, 2022, Big Grove Company collected $9.8 million cash from customers for products that would be delivered in January 2023. Based on the information provided, please answer the following question: As of the fiscal year ended December 31, 2022, what should Big Grove Company report related to the $9.8 million collected from customers?

A. No balance should be recorded as of December 31, 2022.

B. Revenues of $9.8 million

C. Receivable of $9.8 million

D. Liability of $9.8 million

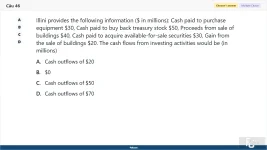

46. (Choose 1 answer)

Illini provides the following information ($ in millions): Cash paid to purchase equipment $30, Cash paid to buy back treasury stock $50, Proceeds from sale of buildings $40, Cash paid to acquire available-for-sale securities $30, Gain from the sale of buildings $20. The cash flows from investing activities would be (in millions)

A. Cash outflows of $20

B. $0

C. Cash outflows of $50

D. Cash outflows of $70

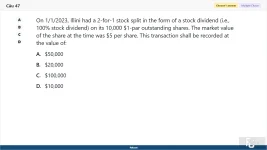

47. (Choose 1 answer)

On 1/1/2023, Illini had a 2-for-1 stock split in the form of a stock dividend (i.e., 100% stock dividend) on its 10,000 $1-par outstanding shares. The market value of the share at the time was $5 per share. This transaction shall be recorded at the value of:

A. $50,000

B. $20,000

C. $100,000

D. $10,000

Đính kèm

-

FIN306c SP26 FE RE_26.webp35 KB · Lượt xem: 2

FIN306c SP26 FE RE_26.webp35 KB · Lượt xem: 2 -

FIN306c SP26 FE RE_01.webp59.2 KB · Lượt xem: 2

FIN306c SP26 FE RE_01.webp59.2 KB · Lượt xem: 2 -

FIN306c SP26 FE RE_02.webp27.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_02.webp27.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_03.webp47.9 KB · Lượt xem: 1

FIN306c SP26 FE RE_03.webp47.9 KB · Lượt xem: 1 -

FIN306c SP26 FE RE_04.webp44.1 KB · Lượt xem: 1

FIN306c SP26 FE RE_04.webp44.1 KB · Lượt xem: 1 -

FIN306c SP26 FE RE_05.webp67.2 KB · Lượt xem: 1

FIN306c SP26 FE RE_05.webp67.2 KB · Lượt xem: 1 -

FIN306c SP26 FE RE_06.webp66.7 KB · Lượt xem: 1

FIN306c SP26 FE RE_06.webp66.7 KB · Lượt xem: 1 -

FIN306c SP26 FE RE_07.webp39.4 KB · Lượt xem: 1

FIN306c SP26 FE RE_07.webp39.4 KB · Lượt xem: 1 -

FIN306c SP26 FE RE_08.webp38.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_08.webp38.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_09.webp46.7 KB · Lượt xem: 0

FIN306c SP26 FE RE_09.webp46.7 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_10.webp37.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_10.webp37.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_11.webp40 KB · Lượt xem: 0

FIN306c SP26 FE RE_11.webp40 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_12.webp112.9 KB · Lượt xem: 0

FIN306c SP26 FE RE_12.webp112.9 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_13.webp29.9 KB · Lượt xem: 0

FIN306c SP26 FE RE_13.webp29.9 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_14.webp39.1 KB · Lượt xem: 0

FIN306c SP26 FE RE_14.webp39.1 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_15.webp28.5 KB · Lượt xem: 0

FIN306c SP26 FE RE_15.webp28.5 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_16.webp68.7 KB · Lượt xem: 0

FIN306c SP26 FE RE_16.webp68.7 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_17.webp98.8 KB · Lượt xem: 0

FIN306c SP26 FE RE_17.webp98.8 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_18.webp28.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_18.webp28.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_19.webp59.3 KB · Lượt xem: 0

FIN306c SP26 FE RE_19.webp59.3 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_20.webp57.1 KB · Lượt xem: 0

FIN306c SP26 FE RE_20.webp57.1 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_21.webp37.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_21.webp37.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_22.webp41.9 KB · Lượt xem: 0

FIN306c SP26 FE RE_22.webp41.9 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_23.webp43 KB · Lượt xem: 0

FIN306c SP26 FE RE_23.webp43 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_24.webp43.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_24.webp43.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_25.webp76.3 KB · Lượt xem: 0

FIN306c SP26 FE RE_25.webp76.3 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_27.webp96.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_27.webp96.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_28.webp55.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_28.webp55.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_29.webp41.8 KB · Lượt xem: 0

FIN306c SP26 FE RE_29.webp41.8 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_30.webp62.9 KB · Lượt xem: 0

FIN306c SP26 FE RE_30.webp62.9 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_31.webp32.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_31.webp32.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_32.webp60.5 KB · Lượt xem: 0

FIN306c SP26 FE RE_32.webp60.5 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_33.webp34.7 KB · Lượt xem: 0

FIN306c SP26 FE RE_33.webp34.7 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_34.webp42.1 KB · Lượt xem: 0

FIN306c SP26 FE RE_34.webp42.1 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_35.webp38.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_35.webp38.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_36.webp52.2 KB · Lượt xem: 0

FIN306c SP26 FE RE_36.webp52.2 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_37.webp69.5 KB · Lượt xem: 0

FIN306c SP26 FE RE_37.webp69.5 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_38.webp48.8 KB · Lượt xem: 0

FIN306c SP26 FE RE_38.webp48.8 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_39.webp31.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_39.webp31.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_40.webp71.6 KB · Lượt xem: 0

FIN306c SP26 FE RE_40.webp71.6 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_41.webp56.3 KB · Lượt xem: 0

FIN306c SP26 FE RE_41.webp56.3 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_42.webp43.5 KB · Lượt xem: 0

FIN306c SP26 FE RE_42.webp43.5 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_43.webp68.3 KB · Lượt xem: 0

FIN306c SP26 FE RE_43.webp68.3 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_44.webp46.9 KB · Lượt xem: 0

FIN306c SP26 FE RE_44.webp46.9 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_45.webp61.8 KB · Lượt xem: 0

FIN306c SP26 FE RE_45.webp61.8 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_46.webp51.5 KB · Lượt xem: 0

FIN306c SP26 FE RE_46.webp51.5 KB · Lượt xem: 0 -

FIN306c SP26 FE RE_47.webp38.8 KB · Lượt xem: 2

FIN306c SP26 FE RE_47.webp38.8 KB · Lượt xem: 2