- Học kỳ

- SP2026

- Thời Gian

- 5/5/26

- Loại tài liệu

- FE

ACC101 SP26 B5 FE RE

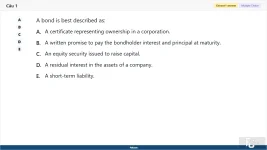

1. (Choose 1 answer)

A bond is best described as:

A. A certificate representing ownership in a corporation.

B. A written promise to pay the bondholder interest and principal at maturity.

C. An equity security issued to raise capital.

D. A residual interest in the assets of a company.

E. A short-term liability.

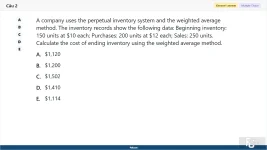

2. (Choose 1 answer)

A company uses the perpetual inventory system and the weighted average method. The inventory records show the following data: Beginning inventory: 150 units at $10 each; Purchases: 200 units at $12 each; Sales: 250 units. Calculate the cost of ending inventory using the weighted average method.

A. $1,120

B. $1,200

C. $1,502

D. $1,410

E. $1,114

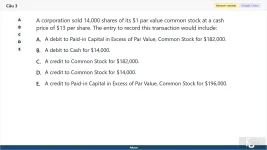

3. (Choose 1 answer)

A corporation sold 14,000 shares of its $1 par value common stock at a cash price of $13 per share. The entry to record this transaction would include:

A. A debit to Paid-in Capital in Excess of Par Value, Common Stock for $182,000.

B. A debit to Cash for $14,000.

C. A credit to Common Stock for $182,000.

D. A credit to Common Stock for $14,000.

E. A credit to Paid-in Capital in Excess of Par Value, Common Stock for $196,000.

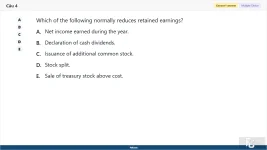

4. (Choose 1 answer)

Which of the following normally reduces retained earnings?

A. Net income earned during the year.

B. Declaration of cash dividends.

C. Issuance of additional common stock.

D. Stock split.

E. Sale of treasury stock above cost.

5. (Choose 1 answer)

Changes in accounting estimates are:

A. Considered accounting errors.

B. Reported as prior period adjustments.

C. Accounted for with a cumulative "catch-up" adjustment.

D. Extraordinary items.

E. Accounted for in current and future periods.

6. (Choose 1 answer)

Closing entries are posted:

A. Before preparing the adjusted trial balance

B. After preparing the financial statements

C. Before preparing the income statement

D. At the same time as adjusting entries

7. (Choose 1 answer)

Net realizable value is:

A. Original cost

B. Estimated selling price minus costs to complete and sell

C. Replacement cost

D. Market price

8. (Choose 1 answer)

What is required when recognizing credit sales?

A. Credit sales are recorded by debiting the bank account.

B. Credit sales are recorded by debiting Accounts Receivable.

C. Credit sales are recorded by crediting Sales.

D. Credit sales are recorded by debiting Sales.

9. (Choose 1 answer)

How is a change in the estimated useful life or salvage value of an asset treated?

A. It is applied to all previous years

B. It affects only future depreciation

C. It results in a loss on the income statement

D. It is recorded as a capital expenditure

10. (Choose 1 answer)

If the market rate of interest exceeds the stated rate of a bond, the bond will sell:

A. At par value.

B. At a premium.

C. At a discount.

D. Above maturity value.

E. Not sell at all.

11. (Choose 1 answer)

On December 1, Victoria Company signed a 90-day, 6% note payable, with a par value of $15,000. What amount of interest expense is accrued at December 31 on the note?

A. $0

B. $75

C. $900

D. $225

E. $300

12. (Choose 1 answer)

Sales returns and allowances

A. Increase revenue

B. Decrease revenue

C. Increase inventory

D. Have no effect

13. (Choose 1 answer)

Which financial statement shows ending inventory for a merchandiser?

A. Income Statement

B. Statement of Retained Earnings

C. Balance Sheet

D. Cash Flow Statement

14. (Choose 1 answer)

The total amount of cash and other assets received by a corporation from its stockholders in exchange for its stock is

A. Always equal to its par value.

B. Always equal to its stated value.

C. Referred to as paid-in capital.

D. Referred to as retained earnings.

E. Always below its stated value.

15. (Choose 1 answer)

Which of the following appears on the income statement?

A. Cash

B. Accounts Payable

C. Service Revenue

D. Retained Earnings

16. (Choose 1 answer)

How do companies use the Percent of Sales Method for estimating bad debts?

A. By multiplying total sales by a set percentage of uncollectibility.

B. By multiplying total accounts receivable by a set percentage.

C. By applying aging categories to past-due accounts.

D. By adjusting the allowance for doubtful accounts each year.

17. (Choose 1 answer)

A periodic inventory system updates inventory:

A. After every sale

B. Only at the end of the period

C. Daily

D. Weekly

18. (Choose 1 answer)

A patent is amortized over:

A. Its legal life or useful life, whichever is shorter

B. Always 20 years

C. Legal life only

D. Useful life only

19. (Choose 1 answer)

Closing entries are recorded:

A. Before adjusting entries

B. After financial statements

C. At the beginning of the period

D. During purchases

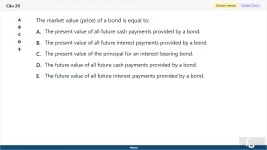

20. (Choose 1 answer)

The market value (price) of a bond is equal to:

A. The present value of all future cash payments provided by a bond.

B. The present value of all future interest payments provided by a bond.

C. The present value of the principal for an interest-bearing bond.

D. The future value of all future cash payments provided by a bond.

E. The future value of all future interest payments provided by a bond.

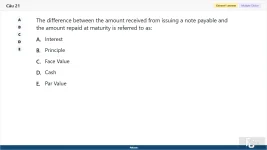

21. (Choose 1 answer)

The difference between the amount received from issuing a note payable and the amount repaid at maturity is referred to as:

A. Interest

B. Principle

C. Face Value

D. Cash

E. Par Value

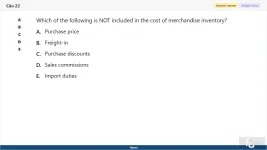

22. (Choose 1 answer)

Which of the following is NOT included in the cost of merchandise inventory?

A. Purchase price

B. Freight-in

C. Purchase discounts

D. Sales commissions

E. Import duties

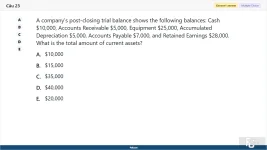

23. (Choose 1 answer)

A company's post-closing trial balance shows the following balances: Cash $10,000, Accounts Receivable $5,000, Equipment $25,000, Accumulated Depreciation $5,000, Accounts Payable $7,000, and Retained Earnings $28,000. What is the total amount of current assets?

A. $10,000

B. $15,000

C. $35,000

D. $40,000

E. $20,000

24. (Choose 1 answer)

When applying the lower of cost or market (LCM) rule, which of the following is considered the "market" value?

A. Replacement cost

B. Sales price

C. Cost of production

D. Original purchase price

E. Future sales value

25. (Choose 1 answer)

What does the Days' Sales Uncollected ratio measure?

A. The total sales in a period

B. The amount of receivables expected to be collected within a year

C. The average days of sales that remain uncollected

D. The number of sales completed during the month

26. (Choose 1 answer)

The right of common shareholders to purchase their proportional share of any common stock later issued by the corporation is called a:

A. Preemptive right

B. Proxy right

C. Right to call

D. Financial leverage

E. Voting right

27. (Choose 1 answer)

Under the lower-of-cost-or-market rule, if market < cost:

A. Record inventory at cost

B. Record inventory at market

C. Ignore difference

D. Debit cash, credit inventory

28. (Choose 1 answer)

Which of the following best explains why unearned revenue is classified as a liability?

A. It represents income earned but not yet received in cash.

B. It is an obligation to provide goods or services in the future.

C. It reduces retained earnings immediately.

D. It is recorded as an expense.

E. It is recorded as an asset until earned.

29. (Choose 1 answer)

A bond is issued at par value when:

A. The bond pays no interest.

B. The bond is not between interest payment dates.

C. Straight line amortization is used by the company.

D. The market rate of interest is the same as the contract rate of interest.

E. The bond is callable.

30. (Choose 1 answer)

When merchandise is sold on account, the perpetual system records:

A. Debit Accounts Receivable, Credit Sales; Debit Cost of Goods Sold, Credit Inventory

B. Debit Accounts Receivable, Credit Inventory

C. Debit Cash, Credit Sales

D. Debit Sales, Credit Accounts Receivable

31. (Choose 1 answer)

Goods in transit shipped FOB shipping point are:

A. Owned by the buyer

B. Owned by the seller

C. Not counted in inventory

D. Included in both seller's and buyer's inventory

32. (Choose 1 answer)

The primary purpose of a merchandising business is to:

A. Provide services

B. Sell goods for profit

C. Manufacture products

D. Invest in stocks

33. (Choose 1 answer)

A company using a periodic inventory system had a beginning inventory of $20,000. During the period, they purchased merchandise worth $60,000. At the end of the period, the physical count of inventory was $15,000. Calculate the cost of goods sold for the period.

A. $75,000

B. $65,000

C. $60,000

D. $55,000

E. $45,000

34. (Choose 1 answer)

The purpose of closing entries is to:

A. Prepare the accounts for the next period

B. Adjust the trial balance

C. Record external transactions

D. Update permanent accounts

35. (Choose 1 answer)

Which of the following statements regarding liabilities is not true?

A. A liability is a probable future payment of assets or services

B. Unearned future wages to be paid to employees should be recorded as liabilities

C. For a liability to be reported, it must be a present obligation that results from a past transaction or event and requires a future payment of assets or services

D. Information about liabilities is more useful when the balance sheet identifies them as either current or long term

E. Liabilities can involve uncertainty in whom to pay

36. (Choose 1 answer)

Which of the following statements is correct about the credit sale?

A. Credit sales are recorded by crediting an Accounts Receivable.

B. As long as a company accurately records total credit sales information, it is not necessary to have separate accounts for specific customers

C. If a customer owes interest on accounts receivable, Interest Revenue is debited and Accounts Receivable is credited

D. Accounts receivable occur from credit sales to customers

37. (Choose 1 answer)

Daily deposits of all cash receipts help reduce which major risk?

A. Overpayment of expenses

B. Loss or theft of cash before deposit

C. Bank reconciliation delays

D. Excess cash balances

38. (Choose 1 answer)

Extracting natural resources increases:

A. Plant asset value

B. Inventory

C. Intangible asset value

D. Depletion expense only

39. (Choose 1 answer)

Which of the following should be included in the entry to establish a petty cash fund?

A. A debit to Cash and a credit to Petty Cash.

B. A debit to Cash and a credit to Cash Over and Short.

C. A debit to Petty Cash and a credit to Accounts Receivable.

D. A debit to Petty Cash and a credit to Cash.

40. (Choose 1 answer)

Which financial statement lists assets, liabilities, and equity at a point in time?

A. Income Statement

B. Balance Sheet

C. Statement of Retained Earnings

D. Statement of Cash Flows

41. (Choose 1 answer)

Which statement about no-par value stock is correct?

A. It must have a stated value.

B. It cannot be legally issued in most states.

C. It is not assigned a value per share by the charter.

D. It requires a minimum dividend.

E. It is usually preferred stock.

42. (Choose 1 answer)

What is a primary goal of cash management?

A. Maximize cash balances

B. Plan cash receipts to meet payments when due

C. Delay the collection of receivables

D. Reduce cash disbursements

43. (Choose 1 answer)

How should a company record a $950 credit sale to CompStore?

A. Debit Accounts Receivable - CompStore $950, Credit Sales $950.

B. Debit Accounts Receivable $950, Credit Sales $950.

C. Debit Sales $950, Credit Accounts Receivable $950.

D. Debit Cash $950, Credit Sales $950.

44. (Choose 1 answer)

A check that was outstanding on last period's bank reconciliation was not among the cancelled checks returned by the bank this period. As a result, in preparing this period's reconciliation, the amount of this check should be

A. Added to the book balance of cash.

B. Deducted from the book balance of cash.

C. Deducted from the bank balance of cash.

D. Added to the bank balance of cash.

45. (Choose 1 answer)

At the end of the accounting cycle, the Income Summary account should have a balance of

A. A debit equal to total revenues

B. A credit equal to total expenses

C. Zero

D. A balance carried forward to the next period

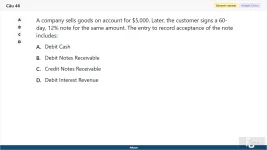

46. (Choose 1 answer)

A company sells goods on account for $5,000. Later, the customer signs a 60-day, 12% note for the same amount. The entry to record acceptance of the note includes:

A. Debit Cash

B. Debit Notes Receivable

C. Credit Notes Receivable

D. Debit Interest Revenue

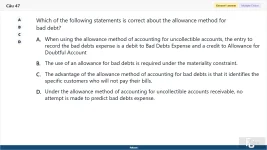

47. (Choose 1 answer)

Which of the following statements is correct about the allowance method for bad debt?

A. When using the allowance method of accounting for uncollectible accounts, the entry to record the bad debts expense is a debit to Bad Debts Expense and a credit to Allowance for Doubtful Account

B. The use of an allowance for bad debts is required under the materiality constraint.

C. The advantage of the allowance method of accounting for bad debts is that it identifies the specific customers who will not pay their bills.

D. Under the allowance method of accounting for uncollectible accounts receivable, no attempt is made to predict bad debts expense.

Đính kèm

-

ACC101 SP26 B5 FE RE_10.webp25.4 KB · Lượt xem: 3

ACC101 SP26 B5 FE RE_10.webp25.4 KB · Lượt xem: 3 -

ACC101 SP26 B5 FE RE_01.webp35.8 KB · Lượt xem: 3

ACC101 SP26 B5 FE RE_01.webp35.8 KB · Lượt xem: 3 -

ACC101 SP26 B5 FE RE_02.webp45.6 KB · Lượt xem: 2

ACC101 SP26 B5 FE RE_02.webp45.6 KB · Lượt xem: 2 -

ACC101 SP26 B5 FE RE_03.webp52 KB · Lượt xem: 2

ACC101 SP26 B5 FE RE_03.webp52 KB · Lượt xem: 2 -

ACC101 SP26 B5 FE RE_04.webp30.9 KB · Lượt xem: 2

ACC101 SP26 B5 FE RE_04.webp30.9 KB · Lượt xem: 2 -

ACC101 SP26 B5 FE RE_05.webp32.7 KB · Lượt xem: 1

ACC101 SP26 B5 FE RE_05.webp32.7 KB · Lượt xem: 1 -

ACC101 SP26 B5 FE RE_06.webp28.3 KB · Lượt xem: 1

ACC101 SP26 B5 FE RE_06.webp28.3 KB · Lượt xem: 1 -

ACC101 SP26 B5 FE RE_07.webp21.9 KB · Lượt xem: 1

ACC101 SP26 B5 FE RE_07.webp21.9 KB · Lượt xem: 1 -

ACC101 SP26 B5 FE RE_08.webp35.1 KB · Lượt xem: 1

ACC101 SP26 B5 FE RE_08.webp35.1 KB · Lượt xem: 1 -

ACC101 SP26 B5 FE RE_09.webp31.6 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_09.webp31.6 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_11.webp30.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_11.webp30.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_12.webp19.1 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_12.webp19.1 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_13.webp25.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_13.webp25.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_14.webp37.7 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_14.webp37.7 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_15.webp21.4 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_15.webp21.4 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_16.webp40.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_16.webp40.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_17.webp20.2 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_17.webp20.2 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_18.webp20.4 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_18.webp20.4 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_19.webp22.4 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_19.webp22.4 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_20.webp45.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_20.webp45.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_21.webp27.2 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_21.webp27.2 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_22.webp25.3 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_22.webp25.3 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_23.webp44.7 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_23.webp44.7 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_24.webp30.3 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_24.webp30.3 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_25.webp33.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_25.webp33.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_26.webp31.5 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_26.webp31.5 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_27.webp24.1 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_27.webp24.1 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_28.webp40.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_28.webp40.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_29.webp33.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_29.webp33.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_30.webp35.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_30.webp35.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_31.webp24.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_31.webp24.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_32.webp22.7 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_32.webp22.7 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_33.webp43.6 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_33.webp43.6 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_34.webp24.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_34.webp24.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_35.webp63.1 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_35.webp63.1 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_36.webp54.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_36.webp54.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_37.webp27.5 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_37.webp27.5 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_38.webp20.6 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_38.webp20.6 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_39.webp38.2 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_39.webp38.2 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_40.webp26.8 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_40.webp26.8 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_41.webp32.5 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_41.webp32.5 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_42.webp27.7 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_42.webp27.7 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_43.webp38.1 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_43.webp38.1 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_44.webp48.5 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_44.webp48.5 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_45.webp30.3 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_45.webp30.3 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_46.webp35.9 KB · Lượt xem: 0

ACC101 SP26 B5 FE RE_46.webp35.9 KB · Lượt xem: 0 -

ACC101 SP26 B5 FE RE_47.webp73.2 KB · Lượt xem: 3

ACC101 SP26 B5 FE RE_47.webp73.2 KB · Lượt xem: 3